》View SMM Copper Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to View SMM Copper Industry Chain Database

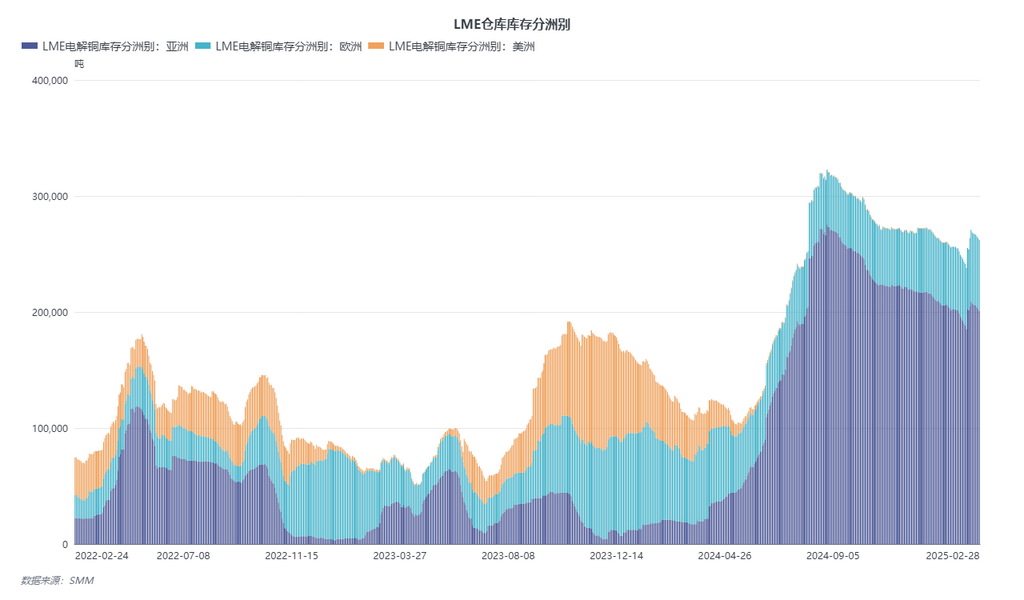

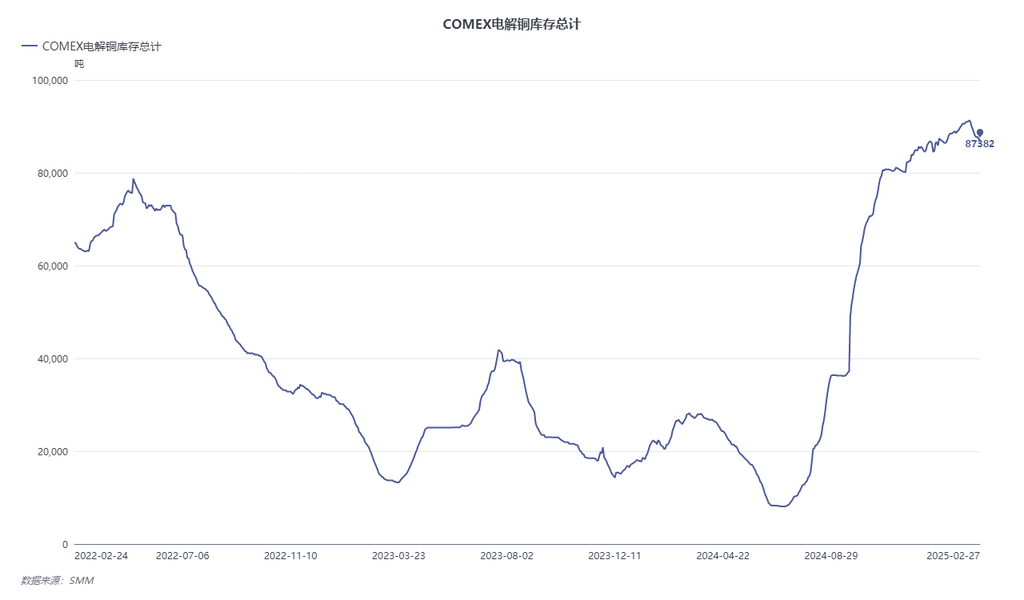

The US tariff policy on copper cathode imports is at a critical turning point. Although no additional tariffs have been imposed yet, the investigation initiated by the Trump administration under Section 232 of the Trade Expansion Act of 1962 has triggered strong market expectations. The core logic of this policy lies in addressing the structural gap in the US domestic supply chain. Currently, the price spread between LME and COMEX copper has set the stage for global trade flows. Following the Trump administration's tariff investigation on copper, the price spread between the LME 3M contract and the COMEX most-traded contract has widened again to around $900-1,000/mt and is expected to persist in the long term before the tariffs are implemented. As a result, the ratio of LME cancelled warrants has reached approximately 30%, and the nearby structure has shifted sharply from the previous contango of around $40/mt to about backwardation of $10/mt. Regarding the dramatic changes in tariffs and overseas market structures, the following are projections of changes in the 2025 spot trade flows of the US dollar-denominated copper market.

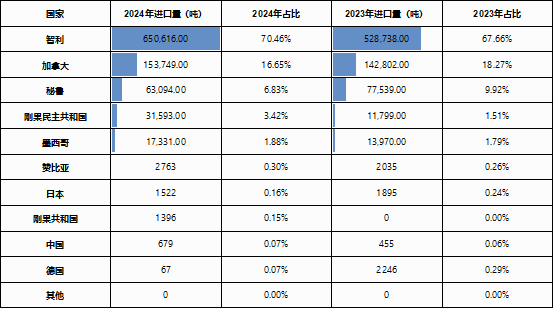

On the one hand, from the perspective of the US domestic market, the US consumes approximately 1.6-1.7 million mt of copper cathode annually, but domestic production is only about 800,000-900,000 mt, with around 50% relying on imports. Among these, Chile is the largest supplier, accounting for 70%, while Canada provides 17% through regional supplementation under the North American Free Trade Agreement.

Currently, the cost of transferring copper cathode from LME Asian delivery warehouses to the US and registering it as COMEX warehouse warrants is approximately $400/mt, with an operational cycle of about 35-60 days. Transporting from Europe to North America costs about $250/mt, with an operational cycle of about 20-35 days. From Africa to North America, the cost is around $300/mt, with a cycle of 25-40 days (subject to fluctuations due to logistics and destination). However, in practical operations, congestion at East Coast ports and inland transportation costs erode about 30% of the price spread profits. Additionally, copper cathode originating from China incurs a 3% trade tariff and a 10% punitive tariff upon customs clearance, while copper cathode originating from Japan incurs a 1% trade tariff. This essentially eliminates the possibility of transferring Chinese and Japanese copper cathode to COMEX warehouses. Currently, trade flows from Asia to North America are mostly short-term speculative. Over a longer timeline, North America's reliance on copper cathode from South America, Africa, and Australia is expected to continue increasing. The significant arbitrage opportunities before the tariffs are implemented also encourage traders to allocate more resources to North America, thereby increasing the trade isolation of the Americas.

On the other hand, the benefits of price spread arbitrage will also lead to a short-term decline in China's imports of copper, exacerbating the tight supply of copper in China. In the Asia-Pacific region, China, with a 55% share of global demand, has established a relatively independent supply network through resource countries such as the DRC, Kazakhstan, and Russia. Since late 2024, imports of copper cathode from South America to China have significantly decreased, and the pricing of long-term contracts in 2025 has further reduced the proportion of South American long-term contracts in imported copper. Amid the tight supply of imported copper concentrates in 2025, the flow of copper in major consumption regions in the Asia-Pacific is expected to become more isolated. Additionally, as the LME structure shifts to backwardation, the financing cost of holding cargo for long-distance trade has risen significantly. Based on the SOFR interest rate, the financing cost per mt of copper cathode is approximately $1.5-1.6/mt/day, losing the cost advantage provided by the deep contango structure of the LME. The activity of long-distance copper cathode trade outside long-term contracts is expected to decline. Undoubtedly, Africa will become one of the most critical regions for resource competition amid the tight supply of copper.

Returning to the domestic imported copper market, in the short term, due to the conflict between weak SHFE/LME price ratio and tight import expectations, the price elasticity of offshore US dollar-denominated copper in the short term has increased, influenced by the price spread between nearby and long-distance sources and the brand attributes of copper cathode from different origins. However, based on current known information: the PASAR smelter in the Philippines has halted production, the Manyar project in Indonesia is unlikely to produce copper before Q3, and routine maintenance at smelters starting in March, coupled with reduced long-distance trade volumes, has made tight import supply a certainty. From Q2 2025, CIF premiums for imported copper are more likely to rise than fall.

In summary, the adjustment of the US tariff policy on copper cathode is driving an accelerated fragmentation of global trade patterns. The widening price spread between COMEX and LME is fostering a decoupled supply chain system between the Americas and the Asia-Pacific. In the short term, cross-regional arbitrage is constrained by logistical bottlenecks and customs clearance costs, while shrinking smelting capacity further exacerbates supply imbalances in the Asia-Pacific. In the long term, regional barriers and resource competition will become the core of pricing. Throughout this process, supply chain security and geopolitical competition will become one of the dominant factors in the new market dynamics.